Rory wants to hear from you!

Share your thoughts about us with our CEO.

For more than 150 years, Mid Penn Bank has been a staple of the community, providing comprehensive financial solutions for individuals and businesses through personalized service and up-to-date products. Whether you visit one of our many financial centers across Pennsylvania or New Jersey or connect with us through online banking, you will see that our top priority is building relationships with our customers and contributing to the vitality of the communities we serve.

Running a business can be a challenge, but the business banking experts at Mid Penn Bank will partner with you to make your business as successful as it can be. We help real estate and construction companies find financing options, assist farming operations in securing agricultural loans, and give businesses in all industries protection against fraud and theft. We also offer:

Preparing for the future requires strategic planning, and our advisors strive to help our customers achieve financial well-being. We offer individualized attention and money management services using time-tested investment strategies. This could mean protecting your assets by putting them into savings, structuring a trust fund, or creating an investment portfolio carefully matched to your risk tolerance. These services include:

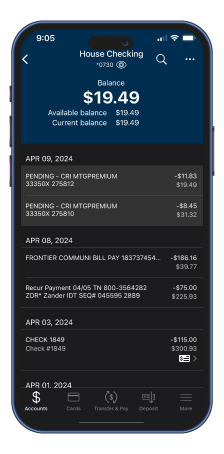

Although we have financial centers conveniently located throughout Pennsylvania and New Jersey, in-person visits are not the only way to bank with us. With Mid Penn Bank Online Banking, you can manage your account, control your cards, pay bills, and make transfers when and where it’s most convenient for you. Our mobile app, telebanking, and digital wallet services allow you to have access to your accounts wherever you go. You can even receive alerts advising you of card activity or when you are getting close to overdrawing your account.

Joining the Mid Penn Bank community connects you with your neighbors in working towards larger goals — like financial freedom, security and economic stability. We’re here to help Pennsylvania and New Jersey grow stronger. Open an account with us today to start enjoying all the benefits you’ll receive for being a trusted member dedicated to growing the community.

You can connect with us at any time to learn more about our services and how you can get started. Get in touch online using our contact form or give our financial centers a call at 1-866-642-7736.

Share your thoughts about us with our CEO.